February 3, 2025

After years of financial turbulence, high costs of borrowing, and deposit outflow, realistically there’s no “normal” for financial services to return to. Experts increasingly accept that volatility is a constant and there’s more grey than black and white.

So, true to form, the coming year is offering few safe bets, but despite the unknowns, consumer spending trends and regulatory shifts are giving lenders reasons for optimism in 2025.

Lower Taxes, Higher Deposits

One potential early win is a swell in consumer tax rebates. The IRS updated its tax brackets late last year and, directly or indirectly, a third of consumers are anticipating higher tax refunds this year than they received in 2024. Key for credit unions is that 43% of consumers plan on boosting their savings with any return.

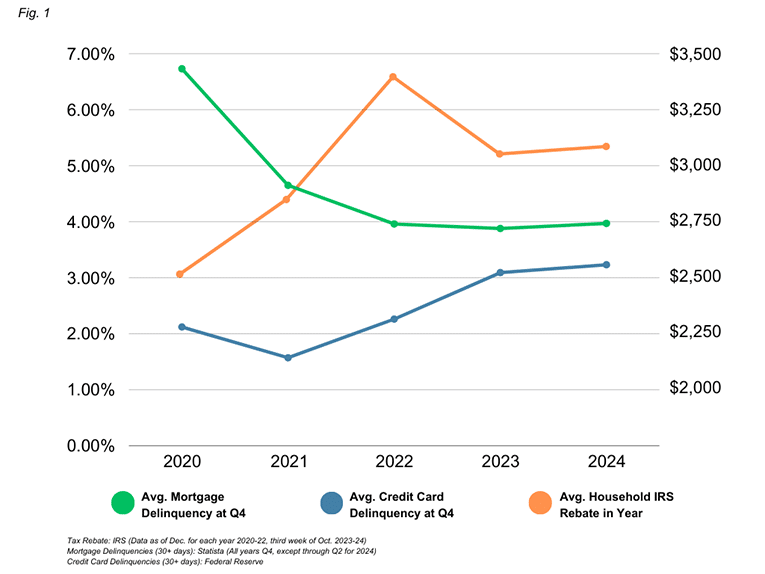

With the average tax rebate breaking $3,000 last year, this could be a huge win for credit unions seeking deposits, right out of the gate—”could” being the operative word.

However, there’s reason for lenders to be optimistic even if rebates don’t lead to an upturn in deposits, as the same study reported nearly half (47%) of respondents would use any return to pay down debt, addressing ongoing concerns about delinquencies.

Delinquencies Still a Concern, but Improvement Expected

Consumers paying down debt would be no bad thing for credit unions either as there’s no denying delinquencies remain higher than ideal.

America’s Credit Unions most recent Monthly Credit Union Estimates report showed the 60+ day delinquency rate grew 0.99% through November 2024—up 19bps year-over-year, and more than a half-a-percent up on the previous month.

However, while Fig 1 shows tax refunds don’t necessarily translate to debt paydown (despite the best intentions) TransUnion’s 2025 Consumer Credit Forecast predicts relief … of sorts. The report anticipates a moderation in credit card balance growth which, yes, will likely coincide with a fifth consecutive year of increased serious delinquencies (90+ days) but a rise of just 2.76% in 2025 would represent a 12bps increase from 2024: A stark contrast to the 78 and 33 basis point increases seen in 2022 and 2023, respectively.

Overall, TransUnion’s projections indicate a return to more typical credit usage; genuinely reason for cautious optimism among lenders.

Embedded Finance and BaaS: The Next Financial Frontier?

With consumers’ seemingly endless appetite for BNPL, a key opportunity for lenders in 2025 is embedded finance.

The good news is, while non-traditional lenders and neobanks are certainly making ever-greater strides into the market, over the last 12 months, credit unions in particular began exploring embedded finance opportunities with greater gusto—particularly to support refinancing in light of the ongoing high-rate environment.

Investing in Banking as a Service (BaaS) programs would enable traditional lenders to reclaim their authority in the space, offering capital services to third parties, opening new revenue streams and expanding their market penetration.

Similarly, whatever your organization’s consumer lending strategy, LendKey’s network lending ecosystem and its integrated loan participation platform are ideally suited to help your institution grow loans and diversify your balance sheet through 2025—a year that’s already looking promising for consumer loans.