March 28, 2025

Sweeping cuts to the Department of Education (DoEd) announced last month were hailed as a significant win for the Trump administration, drastically curtailing the federal body’s remit and reducing its workforce by half.

As with many other executive orders, the DoEd plans were immediately challenged in court, but students and their families can ill-afford to wait for just one ruling among a swell of other active suits. So, what does this mean for students, and could this be a win-win situation for students and a credit union system desperately searching for traction with younger demographics?

Robbing Peter to Pay Paul

At first glance, it could be easy to overlook the growth opportunity posed by these cuts. “Aggregate limits for undergraduate loans will be going from $31,000 to $50,000,” explains student loan expert Mark Kantrowitz, “so there will likely be a decrease in demand for private loans.”

A decrease in demand shouldn’t automatically signify growth for private lenders but look closer. That 61% bump in loan limits is a countermeasure stemming directly from the administration’s plans to eliminate Parent PLUS and Grad PLUS loans.

The PLUS programs have no strict borrowing cap, allowing parents and graduate students to borrow up to the full cost of attendance minus any other aid received. Even among Republican ranks, there’s concern that undergraduates could struggle to finance the full cost of education without those options. Raising undergraduate loan limits offsets that risk … on paper.

Most Impacted Are Lowest Risk Borrowers

“Overall, the PLUS loan programs are about $25.5 billion per year,” Kantrowitz points out. “If those loans go away, you’re going to shift a lot of volume to private lenders.”

More enticing for credit unions is that graduate borrowers typically represent less risk. “This is among the borrowers who are most profitable, least likely to default, and where you can see in advance that they’re going to be low risk.”

Kantrowitz, who has testified before Congress on student lending and financial aid concerns, notes that graduate students and parents typically represent higher-quality credit profiles and that with private student loans currently around $10-12 billion annually, absorbing even a fraction of displaced PLUS borrowers could significantly expand the private lending market.

“Someone getting a PhD in computer science from MIT is extremely low risk. And it’s the lenders, like credit unions, that are best positioned to evaluate the credit quality of these borrowers, not just based on their credit scores and their past repayment behavior, but also their future repayment behavior based on where they’re going to school and what degree they’re pursuing.”

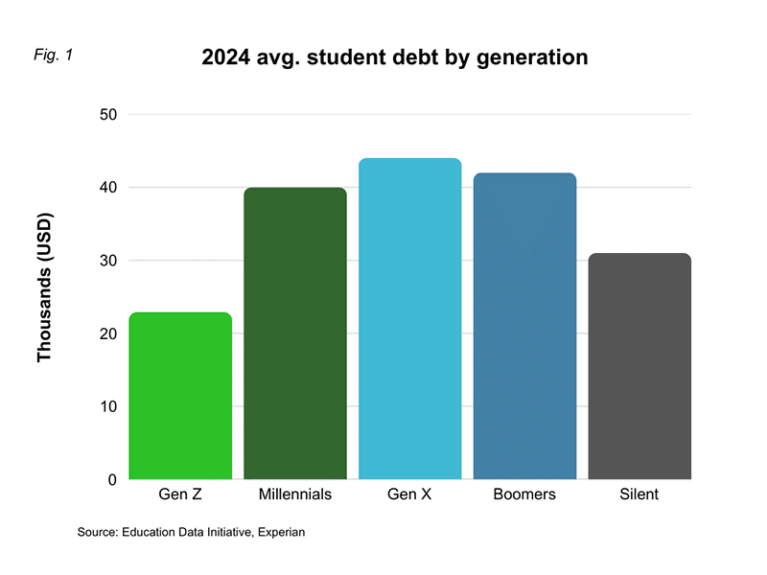

Similarly, data from 2024 (fig 1.) shows that Gen Xers, currently between 45 and 60 years old, hold the highest level of average student debt—debunking any misapprehension that “student” lending is exclusively addressing a younger cohort, not yet in their prime earning (and depositing) years.

Earning the Right to Lend

As federal involvement, interest, and oversight contracts, the opportunity for credit unions to engage younger members—and establish themselves as a long-term, primary financial partner—increases exponentially. The first step is talking the talk.

The DoEd’s massive staffing cuts will likely hit loan forgiveness programs, student support, and the Federal Student Aid ombudsman, leaving an information vacuum that Kantrowitz advises credit unions to fill.

“One of the areas in which credit unions excel is helping their members find answers,” adds Kantrowitz. “If the federal customer service functions are impacted, the credit unions may be able to help their members get answers to their questions. That can be a great way of marketing to their members, ‘Yes, the federal PLUS loans have ended. We have products that can help you, and we can also answer your questions about student financial aid and student loans.'”

Your Partner in Education Lending

Ultimately, the DoEd cuts are universal in their impact. Whether a credit union is actively involved in education lending or not, members, households, and potentially large employee groups will be affected. LendKey is here to help.

Reach out to discover how education lending, refinancing, and servicing can help your credit union in the long term and help millions of members during this turbulent time.