February 28, 2025

This week, with the national credit union system convening in the capital for the Governmental Affairs Conference, there’s seemingly one thing on the agenda: The credit union tax exemption.

Trade association (and GAC host) America’s Credit Unions recently revitalized its ‘Don’t Tax My Credit Union’ campaign in response to renewed fervor among Republican lawmakers who cite the tax exemption—in place since 1937—as a potential source of billions in additional Federal revenue.

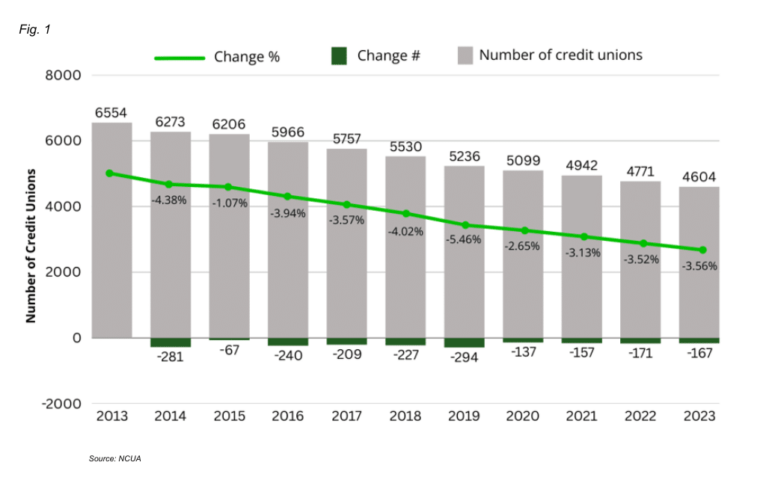

But with credit union numbers in constant decline, two mega-fintech (PayPal and Chime) accounting for one-in-five new checking accounts (fig. 1), and low-to-no engagement with younger consumers, is tax exemption really the fight credit unions should be fighting?

Breaking out of the echo chamber

In a recent 22 Minutes in Lending episode, Brian Kaas made the case for credit unions to prioritize fintech partnerships to ensure long-term survival.

“I’m not going to sugarcoat things,” the president and managing director of TruStage Ventures said, “the world of financial services continues to evolve very rapidly.

“The concern I have is that [credit union events] tend to be comprised of just credit union people. It creates an echo chamber, like, ‘Hey, we’re not doing a whole lot, but I talked to this credit union and they’re really not doing much either, so we must be okay.’” The reality, Kaas argued, is simply not addressed in those interactions.

“You don’t see a lot of credit union folks going to broader fintech conferences to get a feel of just how fast things are changing. I think they’d be blown away by how fast the industry is evolving.”

TruStage Ventures, Kaas explained, is focused on building a platform to help credit unions connect with fintech because “we want to help the industry adapt to the change that’s occurring.”

Rethinking financial products

Ron Shevlin, chief research officer at Cornerstone Advisors, shared a similar perspective. “The typical credit union has maybe 100 years of experience and history, thinking along siloed lines,” Shelvin explained. “It isn’t just a siloed organization. It’s siloed product lines.

“Fintechs, even the larger ones, are designing products to cut across these silos. They’re rethinking the product. This is why it’s so important [for credit unions] to be thinking about the niche you’re focusing on, and what the product needs of that niche is.

“Community banking isn’t dead but the notion of community as geography is on the decline. What’s replacing it is community as affinity.”

Affinity based products that drive deposits

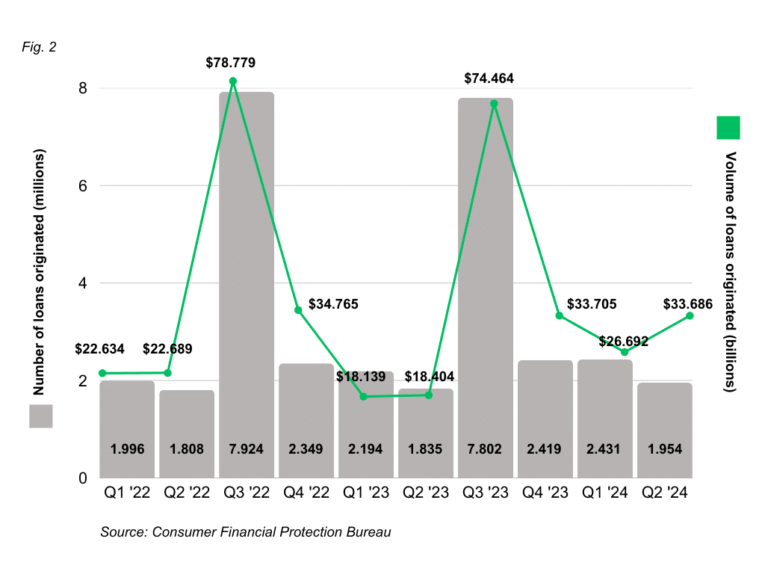

So, if fintech partnerships are the key to credit union survival, and identifying niche markets that credit unions can serve long-term, with cross-pollinating products, will set them apart, where to start? There are certainly higher-risk, lower-reward opportunities than student lending (fig. 2).

In the fourth quarter of 2024, SoFi reported $1.3B in student loan originations—up 71% year-on-year, and the highest volume since the pandemic. This is a market primed for credit unions/fintech disruption.

“It isn’t about student lending for the sake of student lending,” added Shevlin, “it’s student lending for the sake of starting a relationship that’s going to initially bring you deposits. And you grow upon that, and you can own the niche.”

Solving credit union pain points

Of course, there’s no doubt losing the credit union tax exemption would hit credit unions hard, but the exemption exists precisely because credit unions have—and always will, even in the worst-case scenario—placed the wellbeing of their members and communities above profit. Without adopting a more proactive, engaged approach to fintech partnerships, however, things could look a lot worse.